THREE SHORT STEPS TO DECIDE, DESIGN AND FIND YOUR BEST QLAC ELECTION.

INVESTORS LIKE YOU

Decide

Whether QLAC is right for you.

YOUR QLAC

WHAT is a QLAC?

The IRS adopted regulations in July, 2014 (Regulation 401(a)(9)) defining a QLAC and providing

special treatment for it. Specifically, a QLAC is a Qualifying Longevity Annuity Contract

that can be purchased using funds from an IRA or 401(k) and other qualified retirement plans.

Read more

WHAT are specific benefits of a QLAC?

There can be significant advantages to investing in a QLAC:

1. Tax savings on the reduction in RMD payments

2. Income protection - guaranteed income for your life and/or your spouse

3. Enables more aggressive investing of the remainder of your Retirement Account Balance.

Consider the QLAC as the income foundation of your retirement distribution strategy.

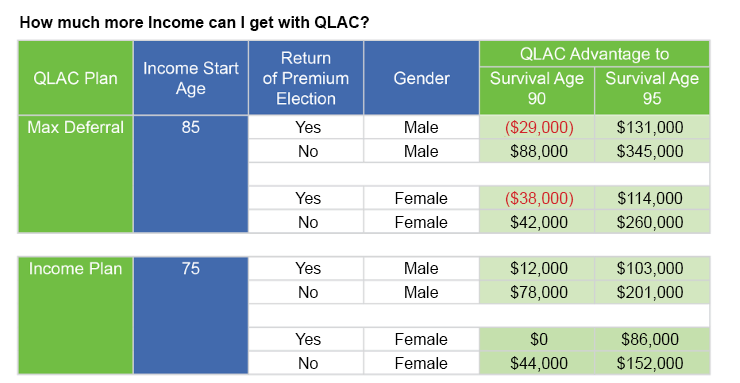

HOW much more income can I get with QLAC?

Allocating funds to a QLAC can generate a sizable amount of additional lifetime income. Each investor's result will depend on the amount invested, his or her unique circumstances, and particularly the survival age. As longevity insurance, the longer an investor lives, the greater the QLAC advantage.

Read more

WHY QLAC MAKES SENSE FOR THE IRS AND YOU?

Why did the IRS adopt regulations permitting the QLAC?

Here's what the IRS said about the rationale for QLAC: "All Americans

deserve security in their later years and need effective tools to

make the most of their hard-earned savings. As boomers approach

retirement and life expectancies increase, longevity income annuities

can be an important option to help Americans plan for retirement and

ensure they have a regular stream of income for as long as they live."

When and why does a QLAC make sense?

Typically, a QLAC makes sense if you're in good health, between ages 60 and 75, and currently have a retirement account balance of $100,000 or over. Also, you must be able to support your current or projected retirement expenses without needing access to the premium used to purchase the QLAC. The chart below shows the maximum amount you could invest in a QLAC.

| Retirement Account Balance | Maximum QLAC Premium | Retirement Account Balance % |

| $100,000 | $25,000 | 25% |

| $400,000 | $100,000 | 25% |

| $1,000,000 | $135,000 | 13.0% |