Frequently Asked Questions

About Income Annuities

Description of Annuities Addressed in This FAQ

There are many types of annuities; however, the focus in this website and FAQ is on the Income Annuity that was first offered in the U.S. more than 100 years ago. It can be defined as a series of guaranteed payments made by a life insurance company, typically on a monthly basis, for the life of the annuitant. The payments may start within 13 months (Immediate Annuity) or start at a later date/age the annuity owner selects (Deferred Income Annuity or QLAC). The savings sources for Income Annuities are very broad (see below).

Within each type of Income Annuity, there are lots of options, including such choices as the form of the annuity payout and beneficiary protection, and hence the need for this FAQ. In addition, in each of the three “shortcuts” in this website there are calculation tools which can enable you to customize your own Income Annuity plan, as well as more background on each type of annuity. You can even have top annuity companies bid on the Income Annuity plan you design for yourself.

| Profile of Income Objectives |

Type of Income Annuity |

Shortcut Link |

|

Ages 60 to 85, Savings in IRA, 401(k), or Other Savings in Personally Held Accounts Want to: Increase and Secure |

Immediate Annuity |

|

Current Income |

Ages 50 to 75, Savings in Personally Held Accounts Want to: Increase and Secure |

Deferred Income Annuity (DIA) |

|

Future Income |

Ages 50 to 75, Savings in IRA,401(k), or Other Qualified Retirement Plans Want to: Defer Taxes and Secure |

QLAC |

|

QLAC Income |

If you'd like to learn more about the differences in these three types of annuities, request an appointment with a Go2Specialist.

Applicable to All Income Annuities

-

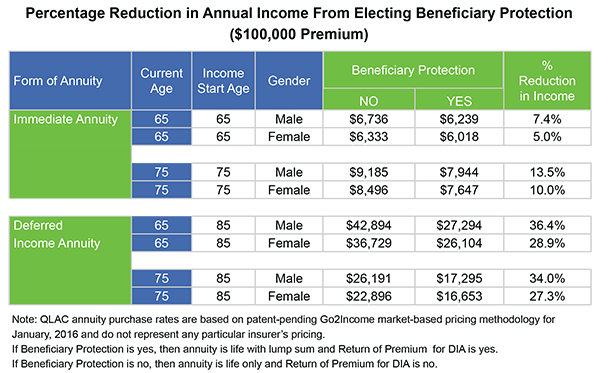

What Does BENEFICIARY PROTECTION Cost?

-

Annuities come in different forms so you can pick and choose the features you want. For example, if you want the maximum amount of lifetime Guaranteed Income, then you'd purchase a life only form of Annuity and your entire premium is going toward protecting your longevity.

In finding premiums to fund your annuity you should generally look for assets where you don't have to realize a taxable gain in order to purchase. Generally that excludes assets with a capital gain, such as a portfolio of stocks or mutual funds.

If your concern is for your beneficiaries in the event of death, then you would want to consider adding beneficiary protection and the choice of lower income for the same premium, or paying a higher premium for the same income amount and still get beneficiary protection. Set out in the table are examples of income with and without Beneficiary Protection.

Applicable to Immediate Annuities

Applicable to Deferred Income Annuities

-

WHEN should you start income under a DIA?

-

When should you start income under a DIA?

If your need is for current income to meet current expenses or to generate a higher cash flow, then a Current Income Annuity makes sense. If, however, you'd like income deferred into the future or you'd like to create your own personalized Income Plan, select a Deferred Income Annuity. If your savings are in a Rollover IRA or qualified and you'd like to replace fluctuating Required Minimum Distributions (RMD) with future guaranteed income you should consider QLAC.

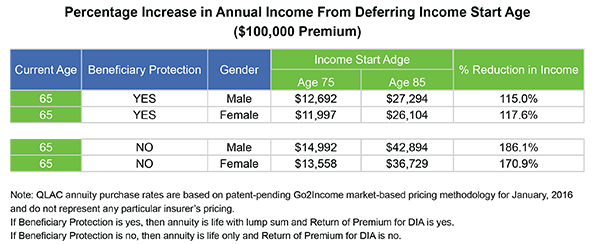

How much more income do I get for delaying the Income Start Age (ISA)?

The chart below shows the increase in income from delaying the DIA's Income Start Age (ISA). The compounding growth comes both from interest and longevity credits. Of course, the ISA should be selected with your personal objectives in mind.