1. If I already own a Single Premium Deferred Annuity (SPDA), should I consider exchanging it for an Income Annuity (IA)?

SPDAs are designed to accumulate your savings on a tax deferred basis. These contracts can be converted into a stream of guaranteed Income whenever you choose to do so.

Insurance and tax laws do not require that you make an exchange with the insurance company that issued your SPDA; therefore, you can and should get competitive quotes from other insurance companies offering Income Annuities.

Several benefits of exchanging your SPDA to an Income Annuity are:

1. Obtaining secure lifetime income

2. Excluding a portion of each payment from tax

3. Locking in long term interest rates

Exchanging an existing SPDA for an Income Annuity may also impact other factors, such as liquidity, so exchanges should be done with considerable thought.

If you’d like to discuss this further or get annuity quotes, please request an appointment with a Go2Specialist.

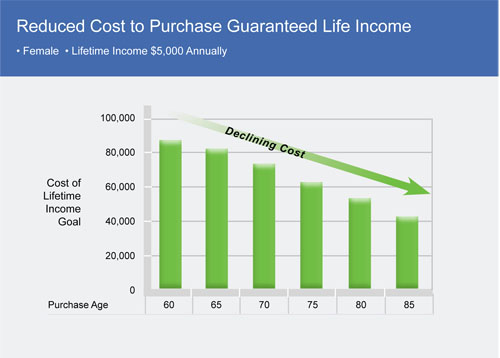

2. Should I consider staging the purchase of annuities as some financial pundits recommend?

As the chart below shows, the cost of purchasing a fixed amount of income decreases as you get older. That pattern is simply a byproduct of the decline in life expectancies that come with age. Deciding whether to stage these purchases is an important decision, one that a Go2Specialist would be happy to discuss it with you.

Note: Based on Go2Income Analytics as of April, 2024

If you’d like to discuss this further, please request an appointment with a Go2Specialist.

3. How would I pay for an annuity?

Generally speaking you write a personal check for an annuity, since you can't swap securities or an investment

account for an annuity. However, there are several important situations in which you can simply

exchange your investment(s) for one or more annuities with:

- Rollover of the assets in a Rollover IRA, 401(k) or other qualified employer plan

- 1035 exchange* of any form of deferred annuity - in full or in part.

- 1035 exchange* of cash value of a life insurance policy (but only if a death benefit is

no longer needed)

* Section 1035 of the Internal Revenue Code

If you’d like to discuss this further, please request an appointment with a Go2Specialist.

4. Should I consider an Income Annuity that increases by a fixed percentage rather than one tied to the Consumer Price Index (CPI)?

Some annuities provide income payments that increase each year by any changes in the cost of living, usually subject to an increase maximum in any given year. For the equivalent premium and type of annuity, you start receiving lower payments. It will take a number of years for these increasing payments to begin to exceed the level payments you would have otherwise received from an annuity offering no such cost of living increases.

There are also annuities that increase the income payments by a fixed percentage, such as 2%, 3% or 4% each year.

If you’d like to discuss this further, please request an appointment with a Go2Specialist.

5. Should I consider an Income Annuity that provides a lump sum refund of any amounts still unpaid at death?

Go2Income analytics and charts assume that any such refunds will be paid out in installments to the beneficiary rather than a lump sum. While both methods provide reasonable beneficiary protection, the decision between the two depends more on the how you want any refund paid to your beneficiary, and less on the level of annuity payments.

If you’d like to discuss this further, please request an appointment with a Go2Specialist.

6. What are the considerations for the purchase of an IA at older ages?

Age, your health, and expectations of longevity (yes, your genes do count) should be taken into consideration when purchasing an Income Annuity. In fact, many life insurance companies do not offer annuities to investors over age 80, or if they do, beneficiary protection is required.

Unlike life insurance policies, applications for annuities do not require any underwriting regarding your health. If your health and/or life expectancy is an issue, you may want to consider an annuity with beneficiary protection such as Life with 100% Refund, even if you are not yet age 80.

Also, if health does not a present a problem for your spouse, you could consider a broader range of Income Annuities on the life of your spouse, with or without beneficiary protection.

If you are over age 80, or wish to discuss some of the issues raised above, you can speak directly with a Go2Specialist at 1-877-263-5576 to determine what may be best for you and/or your spouse.

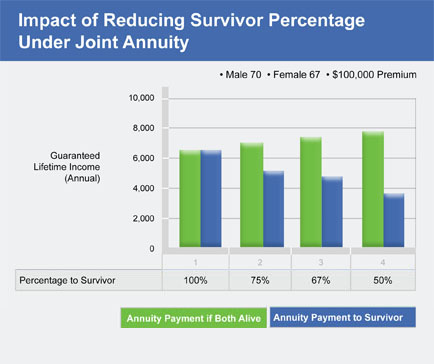

7. To get more starting income under a Joint and Survivor Annuity, should I elect lower income to the surviving annuitant?

The Current Income Shortcut covers annuities that make regular income payments to you, and if the survivor you name (typically a spouse) outlives you, payments continue for his/her lifetime. The income to the surviving spouse can continue at the same level, as illustrated in the website.

If you believe that the surviving annuitant would need less income, choosing this option will increase the income paid while both are alive. The chart adjacent shows that you can increase the joint income by around 12% if you reduce the survivor income by 33% (from 100% to 67%).

Note: Based on Go2Income Analytics as of April, 2024

This is an important decision which requires you to consider future needs of any surviving annuitant.

If you’d like to discuss this further, please request an appointment with a Go2Specialist.

If you’d like to discuss any of these advance topics on this page or review anything else on the Go2Income website, please schedule an appointment with a Go2Specialist.

Click here