How Do I Select the Type of Annuity that Best Fits My Personal Situation?

Most 401(k) plans offer a series of annuity options but little help in assisting you make the right decision. They do require that if you are electing an annuity option you select a special joint and survivor annuity. Under this annuity, the annuity payments only reduce on the death of you the annuitant, not on the death of the survivor annuitant.

When considering an annuity option offered through your employer, you should also shop the commercial annuity market, There may be better rates or and different options to choose from.

If you’re interested in annuities as part of a broader investment program, you might consider rolling to an IRA that permits annuities to be held in the account. Again, an advisor with experience with annuities can help when considering these issues.

How do I Evaluate Alternatives to My Purchase of an Annuity?

It’s challenging, even for most financial advisors, to compare a product like life insurance, long term care insurance or an annuity, to an investment vehicle. Besides the obvious investment and tax differences, the most critical is that “return” under the insurance –issued policies depends on your lifespan and in some cases your health. What we have done is to determine the rate return under the annuity depending on your “survival age”.

While there are many types of plans and schemes that offer streams of retirement income, you have to make begin any comparison by answering the following questions for the alternative:

Is the income guaranteed?

If so, what is the credit rating of the financial institution?

If not, what parameters affect the outcome, such as market returns, interest rates, etc?

Is the income payable for life?

If not, what do you do if that account runs out?

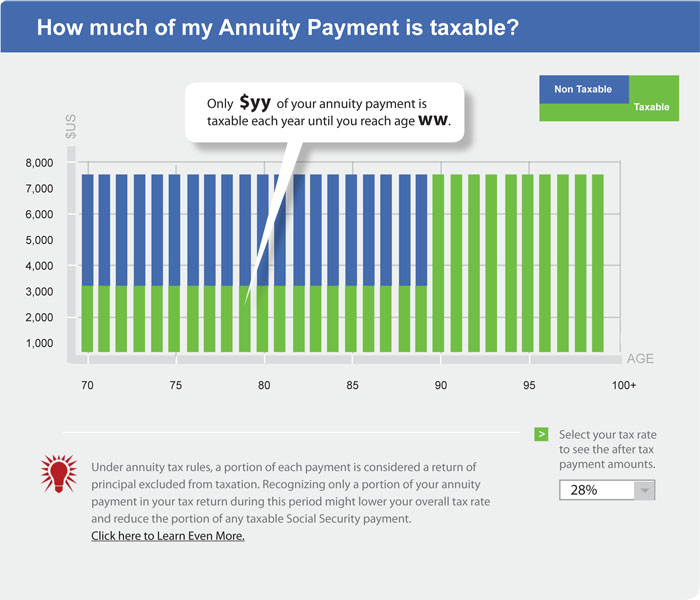

Is a portion of the income treated as a tax free recovery of cost basis?

How Can I Access the Values of My Annuity?

If your annuity has a refund or certain period, the annuity contract has what is known as a commuted value. In most contracts you can withdraw a portion of the commuted value in exchange for a reduction in your payments during the refund or certain period. That withdrawal decision should not be made lightly.

However, as part of a broader financial plan, you might consider borrowing money, and using a portion of your payments as a source of repayment. Of course, you should not borrow beyond the value of payments made during the refund or certain period. Here is an example: An investor (male aged 70) purchases a Life with 100% Refund Annuity for a $100,000 premium. Based on November 2013 pricing, the annuity payment is $7,455 with an assurance that it will be paid. At those interest rates, that’s worth approximately $70,000, which can be accessed through the contract’s commuted value or through external financing. Both should be used sparingly.

How do I Evaluate Alternatives to My Purchase of an Annuity?

It’s challenging, even for most financial advisors, to compare a product like life insurance, long term care insurance or an annuity, to an investment vehicle. Besides the obvious investment and tax differences, the most critical is that “return” under the insurance –issued policies depends on your lifespan and in some cases your health. What we have done is to determine the rate return under the annuity depending on your “survival age”.

While there are many types of plans and schemes that offer streams of retirement income, you have to make begin any comparison by answering the following questions for the alternative:

Is the income guaranteed?

If so, what is the credit rating of the financial institution?

If not, what parameters affect the outcome, such as market returns, interest rates, etc?

Is the income payable for life?

If not, what do you do if that account runs out?

Is a portion of the income treated as a tax free recovery of cost basis?